- Thread starter

- #1

Geems

America First

- 3,232

- 317

- 83

- Joined

- Jan 13, 2017

- Location

- Land of the Free

- Hoopla Cash

- $ 381.82

- Fav. Team #1

- Fav. Team #2

- Fav. Team #3

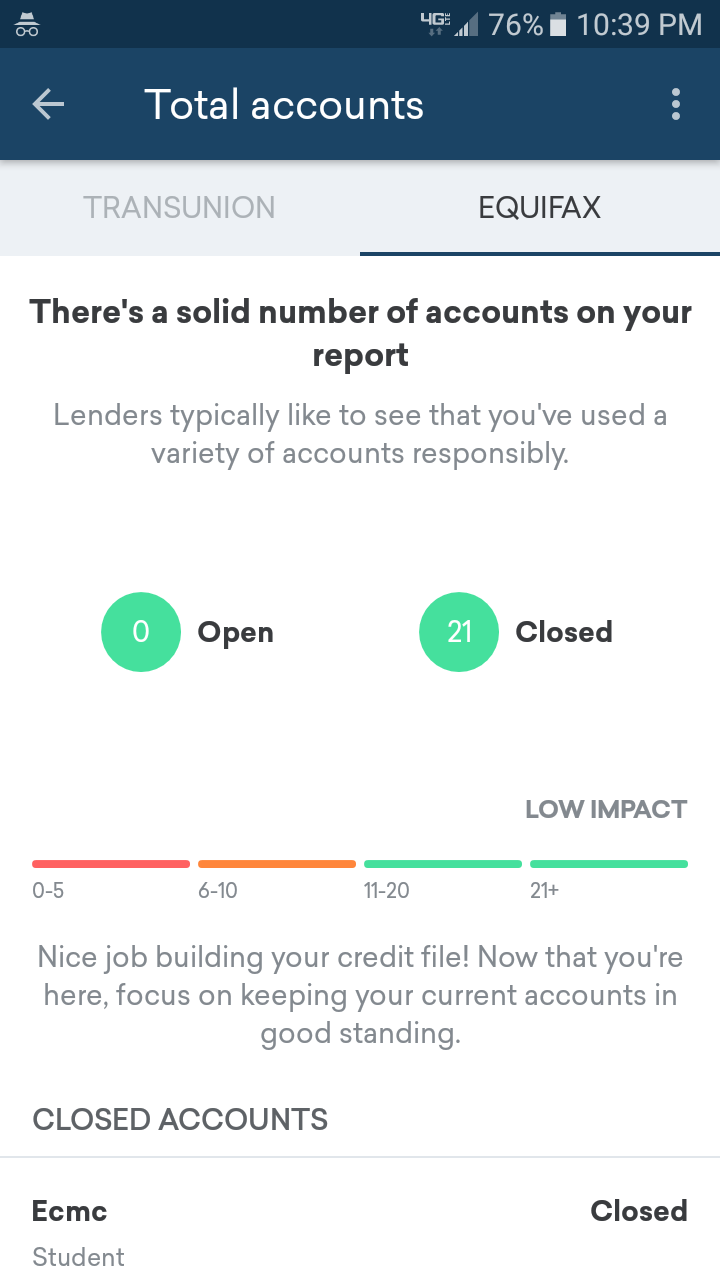

so I've got a shocking 21 accounts listed on my report.

Some ended badly some either ended on good terms or are still open on good terms.

Since total accounts serve an impact on the scores, at one point do they vanish from my report all together?

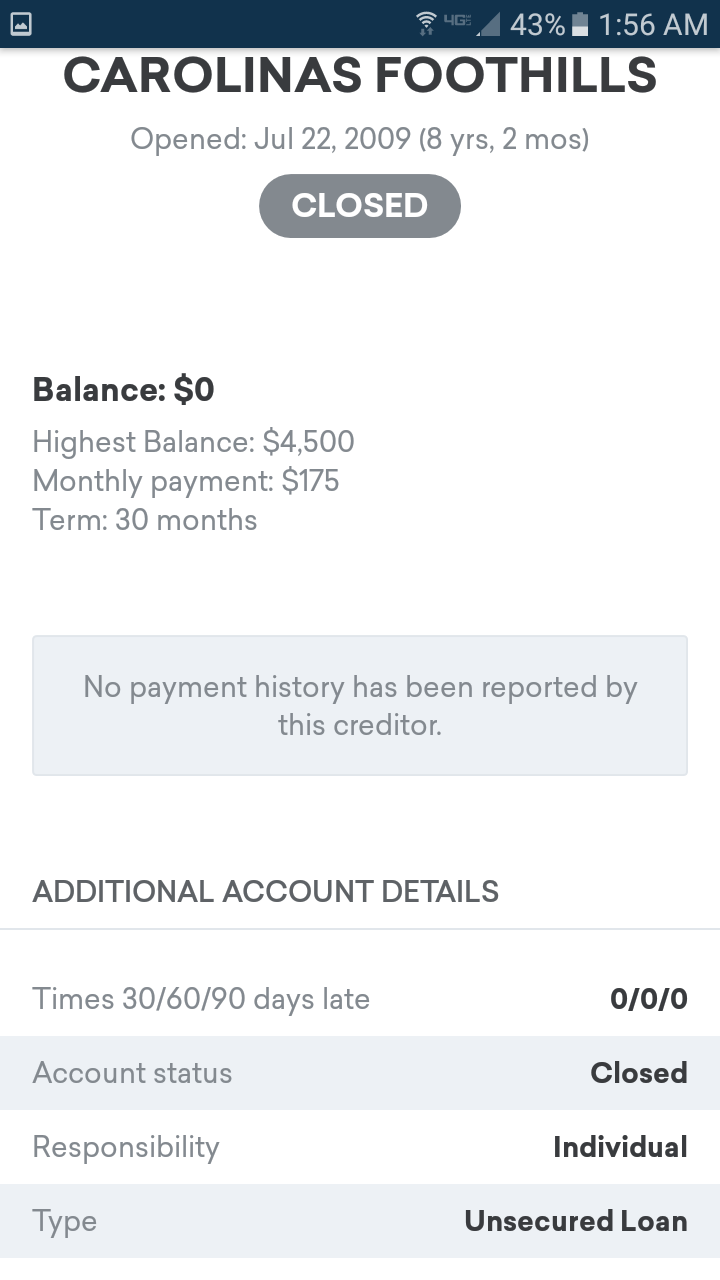

Example: I have a Belk CC that has been paid off and closed back in 2011.

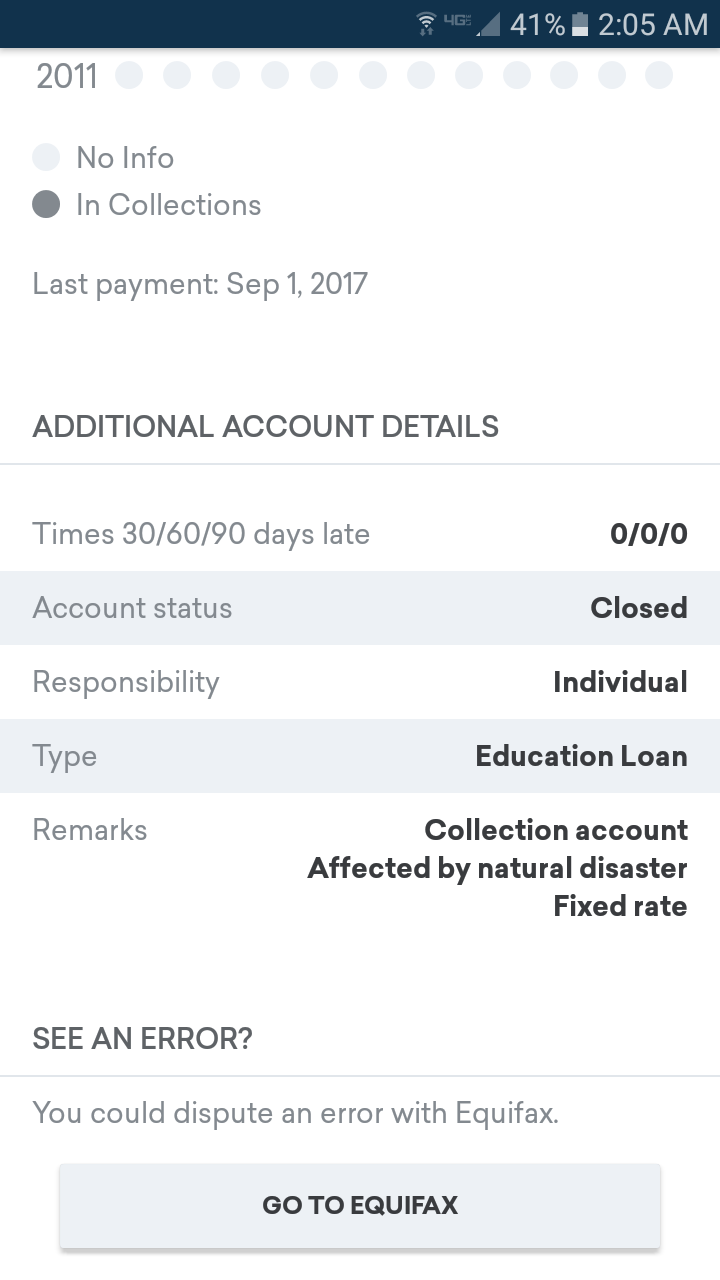

I also have a Capital One CC that I walked away from back in 2015, with money that was owed I never paid.

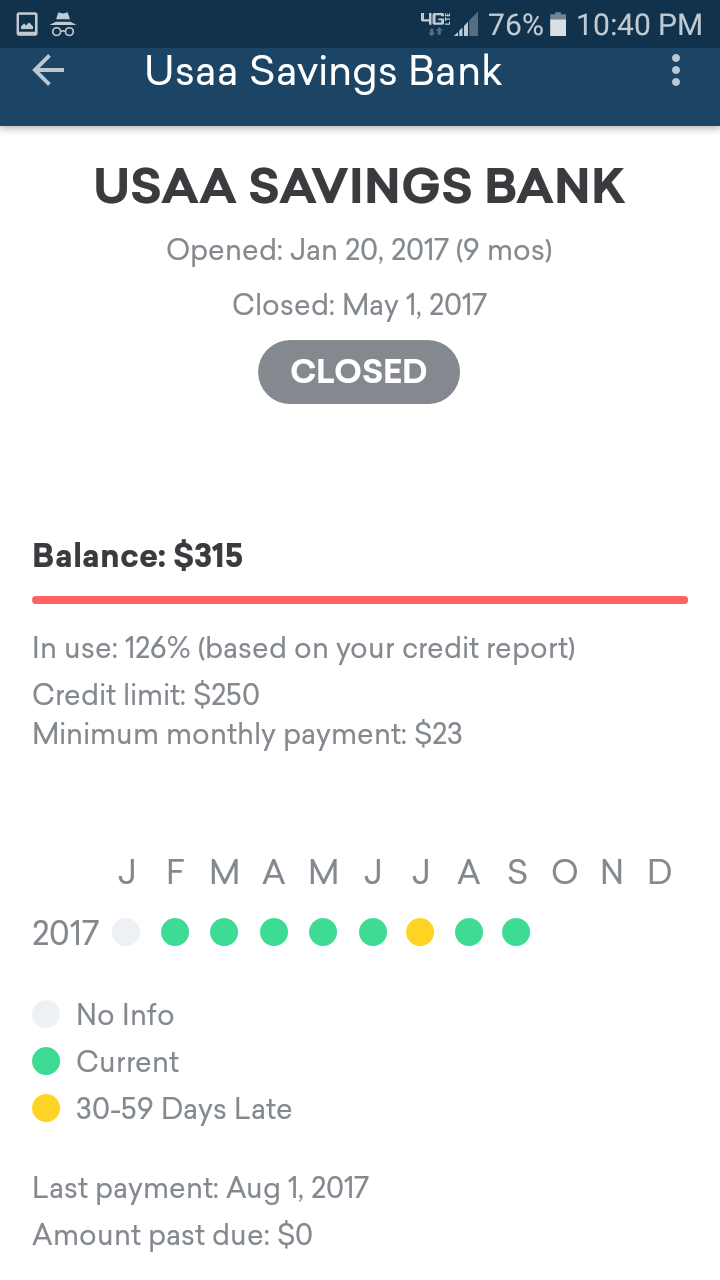

Lastly (for use as my example), I have a USAA secured CC that is current, and for some reason this current acct has the same labelling 'closed'

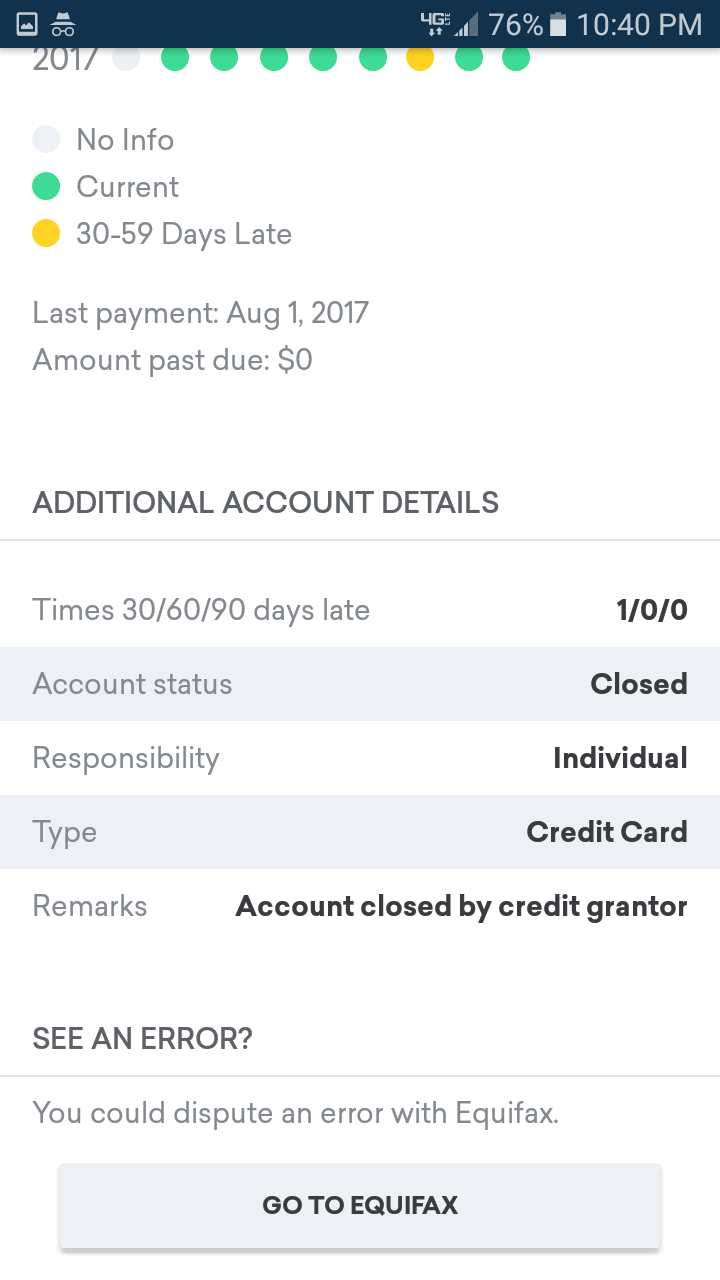

All examples show 'closed' so the question is, when do they fall off? Why are these different accounts seemingly mislabeled?

God dammit why would both a defaulted acct, a paid off acct and an open and current acct all be showing up as 'closed'?

Some ended badly some either ended on good terms or are still open on good terms.

Since total accounts serve an impact on the scores, at one point do they vanish from my report all together?

Example: I have a Belk CC that has been paid off and closed back in 2011.

I also have a Capital One CC that I walked away from back in 2015, with money that was owed I never paid.

Lastly (for use as my example), I have a USAA secured CC that is current, and for some reason this current acct has the same labelling 'closed'

All examples show 'closed' so the question is, when do they fall off? Why are these different accounts seemingly mislabeled?

God dammit why would both a defaulted acct, a paid off acct and an open and current acct all be showing up as 'closed'?